European Union – United States Trade Deal: Poland

On July 27th, the European Union and United States struck a deal which saw the tariff rates set by President Donald Trump at 30% decreased to 15%. As was first announced on April 2nd, Trump had initially planned to set a reciprocal tax of 20% onto the EU via Executive Order 14257. On July 12th, Trump announced the tariff rate for the EU would increase to 30%. This announcement was accompanied by a 90-day deadline extension until August 1st.

As I spent this past summer conducting research in Gdańsk, I was curious as to the effects of this trade agreement on Poland. On the surface, tariffs, in this context, indicate the price of Polish goods increasing in American markets. However, much has been written about tariffs beneath the surface and in hopes of understanding these hidden layers, I decided to perform a quick diagnosis of three different Polish economic pulses and how tariffs may affect these pulses. The first economic pulse is the current Polish business environment as measured by the Polish Economic Institute; the second is the EU-Poland trade dynamics; and finally, Poland’s profile in shifting global trade trends.

How exactly this trade deal will affect the Polish economy is difficult to pinpoint. The Polish prime minister, Donald Tusk, claimed recently that 15% tariff rates would cost Poland 8 billion zł or roughly $2.16 billion. Assuming this is an annual cost, this estimate, according to World Bank Data, would represent around 0.2% of Polish GDP in 2024 at current US$.

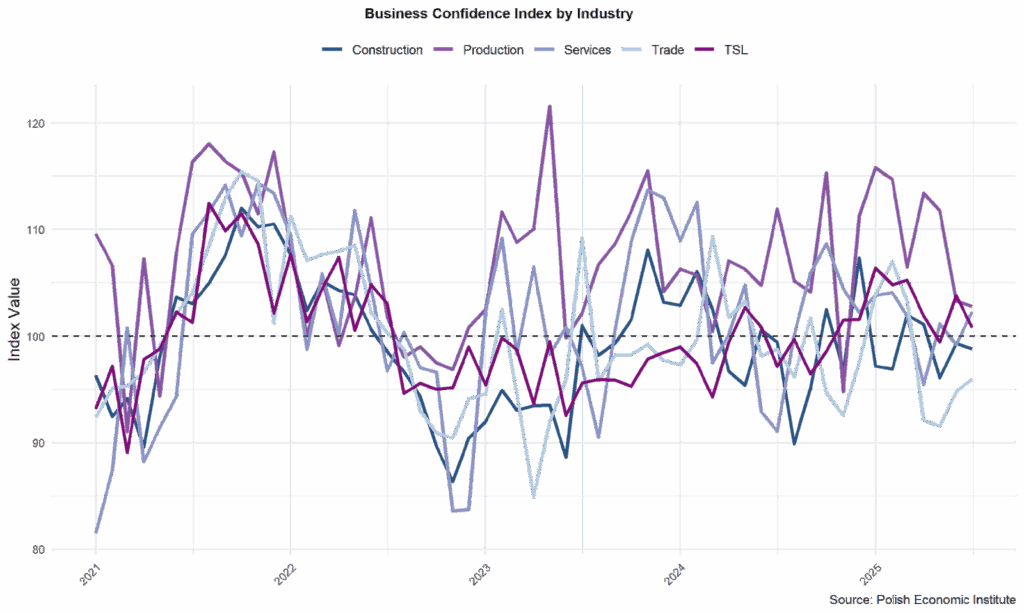

In the lead-up to tariff impositions, the business environment in Poland has sent mixed signals. Observing the Polish Economic Institute’s Miesięczny Indeks Koniunktury (monthly business climate index), visible in Figure 1, since the onset of 2025, the Polish production sector has fallen significantly and approaches the ‘neutral index’ value of 100. Polish construction, trade, and services fell under the neutral index in the first quarter of 2025 and have since risen slightly indicating a ‘negative business mood’.

Figure 1

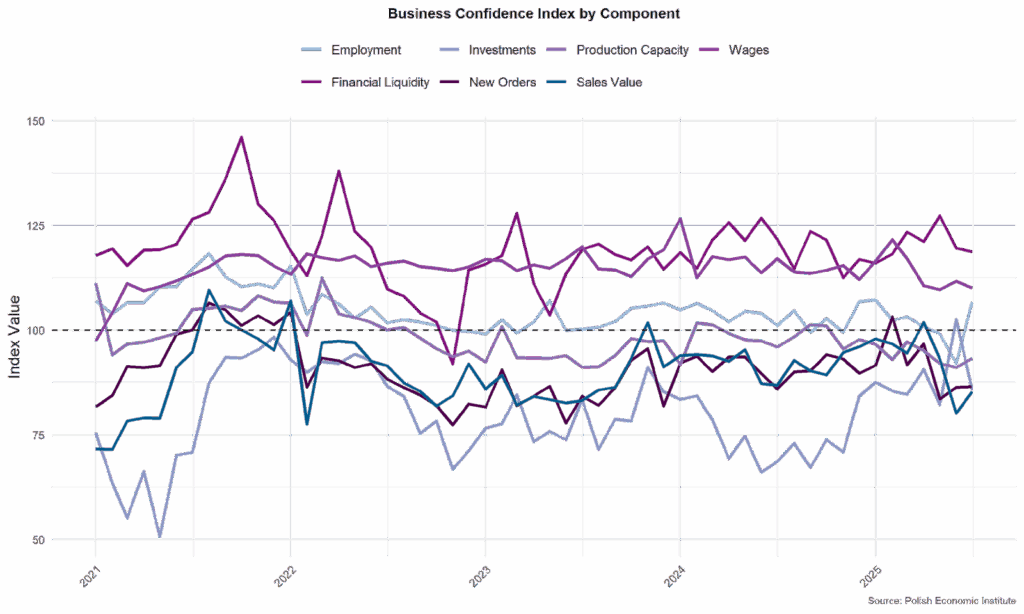

Looking at the Business Components in Figure 2, production capacity, though historically positive, has begun to drop despite initial improvements in 2025. Financial liquidity, too, remains above the neutral index value; however, sales value, new orders, and production capacity appear to struggle despite improving at the beginning of 2025. Updated in July 2025, the data demonstrates increasing preparations for tariffs, notably in production, where a mid-year jump indicates an attempt to supply stockpiling demand. Keeping an eye on these charts through the next months will provide important insight into the key components of the Polish business climate.

Figure 2

The anticipatory trends reflected in the Business Confidence Index may stem from the implied knock-on effect these tariffs will have on the rest of Europe, rather than the effects on direct trade between Poland and the United States. In 2023, Europe alone accounted for 86.34% of Polish exports, indicating that any blow to the larger European economy is passed on to Poland. Compared to Europe, the U.S. accounted for 3.26% of Poland’s exports, or $10.9 billion of goods in 2023. Regardless, Trump’s tariff announcement was mirrored by a downward spike in Polish production and trade.

One key Polish trade partner to monitor in the coming months is Germany. Any blow to Germany, Poland’s largest trade partner, and its auto industry may have more significant effects than direct American tariffs. In 2023, cars and car parts accounted for $22.41 billion of Polish exports and $224 billion of German exports. A slimmer American car market may lead European car manufacturers to sell elsewhere, a goal which could prove difficult given increasingly competitive Asian auto markets.

Zooming further out, tariff dynamics between Asia and the United States may result in a comparative advantage for Polish goods (not necessarily cars) in American markets. As PKO BP chief economist Piotr Bujak points out, many Asian countries face higher American tariff rates than the EU, allowing EU products to remain comparatively cheaper for American consumers. Furthermore, Asian and European economies may look to one another for new markets. As of 2023, Asia accounts for 6.65% of Poland’s exports. If Asian markets prove more profitable, Poland may seek to capitalize on a quickly fluctuating global economy. This would parallel larger European trade shifts eastward towards Asia.

Shifting global currents may bolster Poland’s ability to attract investment as a relatively isolated economy within the European bloc, too. As Poland’s economy boasts year-on-year growth of 3.8% in the first quarter of 2025, 2.4% higher than the EU average, it is beginning to cultivate an identity as a stable destination for foreign investment. One indicator is the Warsaw Stock Exchange General Index (WIG), which has seen 40% growth since last year and a 20% increase since Trump announced EU tariffs in April. Other general indicators, such as the gross government debt-to-GDP ratio of 55%, lower than the EU’s 87% average, and autonomy over interest rates, may fuel investment ahead of an uncertain global economic climate.

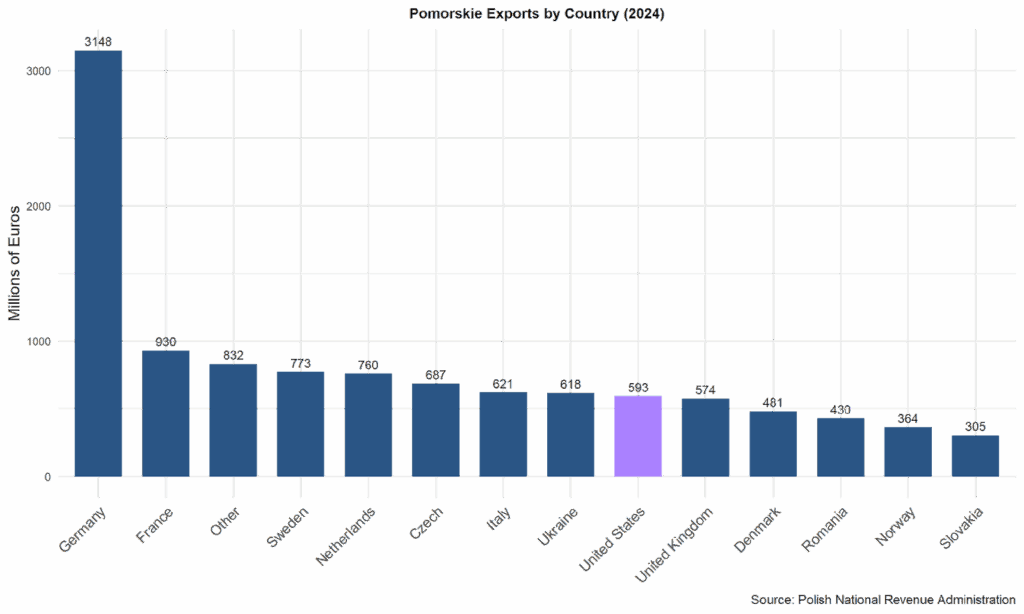

At the regional level, the Pomorskie region remains one of the least exposed regions to American trade. In 2024, as visible in Figure 3, the U.S. accounted for €593 million ($690 million) of Pomorskie exports. The Pomorskie region overwhelmingly relies on Germany as a trade partner, which made up €3,148 million ($3,662 million) of the region’s exports in 2024. France, Sweden, Holland, the Czech Republic and Italy follow as the largest exports to the Pomorskie region, reiterating Poland’s reliance on the EU as its key trade partner.

Figure 3

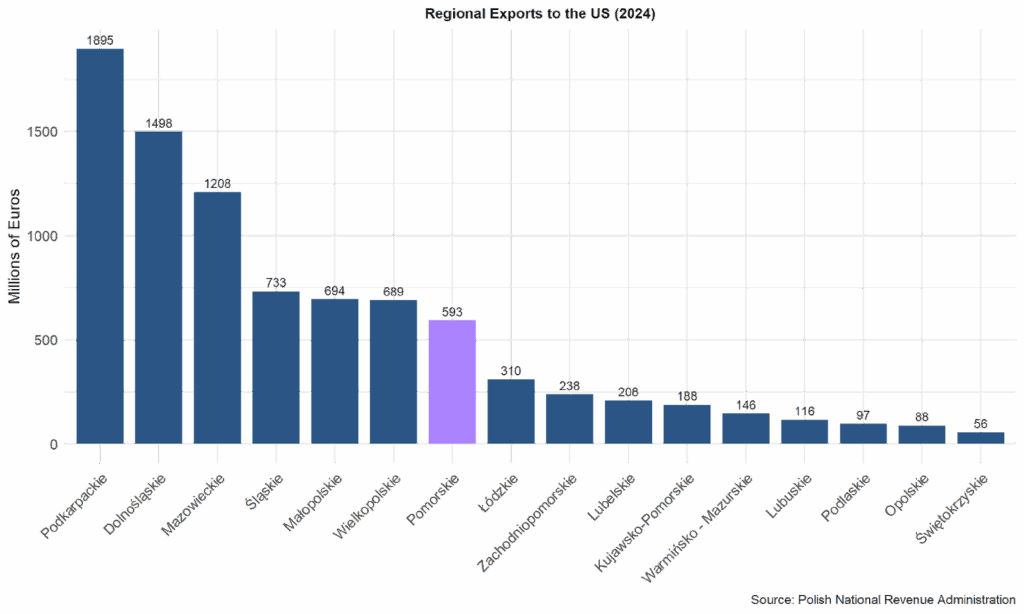

Trade volumes mirror regional economic size. As the 7th largest Polish regional economy, the Pomorskie region is the 7th largest exporter and 8th largest importer of American goods. The largest exporters to the U.S. are the Polish Podkarpackie, Dolnośląskie, and Mazowieckie regions, each exporting over €1,000 million ($1,163 million) of goods to the U.S. in 2024.

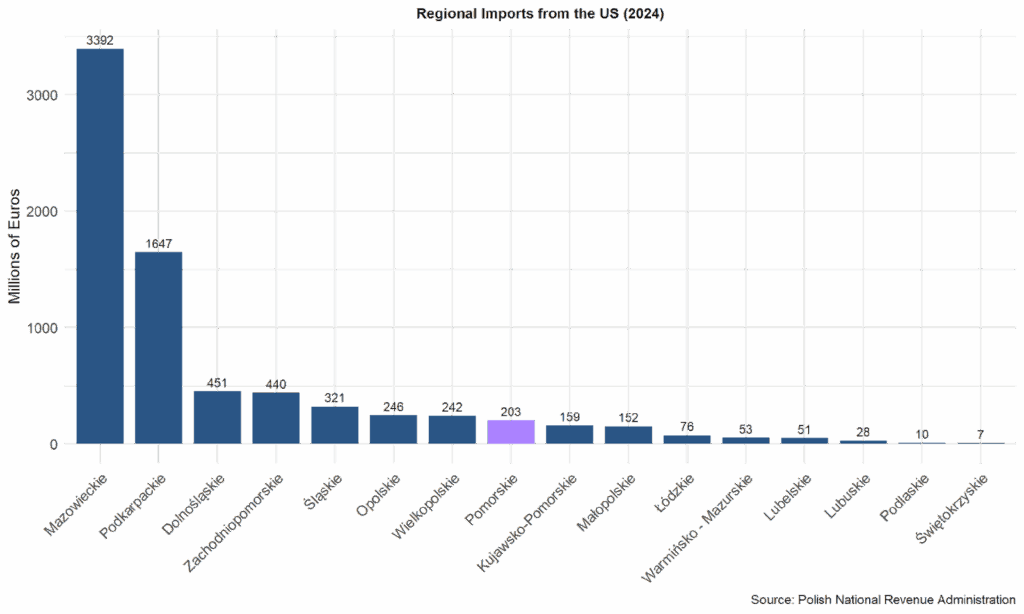

Figure 4

Imports from the U.S. are largely dominated by the Mazowieckie region, wherein Warsaw resides. In 2024, the Mazowieckie region’s American imports totaled €3,392 million ($3,946 million). The Pomorskie region imported considerably less than the Mazowieckie and Podkarpackie regions in 2024.

Figure 5

The auto sector has been subject to 25% tariffs from the Trump administration earlier this year, resulting in losses of $1.5 billion for Volkswagen, $420 million for Mercedes-Benz and $380 million for Stellantis. Continued losses could adversely affect manufacturing plants in Europe. At the regional level, it will be worth following how European industries attempt to buck American tariffs. Volkswagen, Mercedes-Benz and Stellantis all have manufacturing and assembly plants in several parts of Poland, including one Scania (Volkswagen) location in Słupsk, Pomorskie. Oliver Blume, CEO of Volkswagen, has suggested an unorthodox move to negotiate a deal with the Trump administration directly.

Other industries remain subject to tariffs too. While the Pomorskie region is less exposed than other parts of Poland, it is not isolated. How businesses with footholds in Poland and the Pomorskie region react to tariffs will provide the most tangible insight into the regional effects of tariffs. As is the nature of blanket tariffs, many Polish key sectors will likely be affected; however, to what extent remains unclear. Moving forward, all Polish eyes will not only be uncomfortably focused East, but West now, too.